I had a quick visit with Armstrong & Getty this morning to discuss the UHC CEO murder, America’s reaction thereto, why so much of the ire on this topic is off base, Obamacare’s medical loss ratio mandate, the Medicare cost shift, and some super simple advice on purchasing insurance products.

Since 2009, I’ve been on air with Jack and Joe well over 100 times. It's always an honor to be on their show.

Ever imagine healthcare could feel like the Wild West? Welcome to the untamed lands of Reference-Based Pricing (RBP), the sizzling frontier where a select few employers unleash radical savings while giving the traditional PPO system a stiff arm.

Unveil a world where only 3-4% of employers dare to tread, but where jaw-dropping 30-40% savings rain like gold and concierge-level service is the sheriff in town.

Curious about RBP's magic? This isn't just healthcare. It's "Health-FAIR!" Here, employers "price-match" medical costs against benchmark prices, slicing their claims in half compared to big insurers.

Projections say employer healthcare costs will shoot up another 7-9% in 2024. Yet Medicare Part D Premiums are projected to decrease by 1.8%. All major insurers participate in both markets. The lesson? Employers with private insurance are subsidizing Medicare. But hold your horses. With RBP, brace yourself for a 0-2% trend that turns the tables on traditional care.

Jump into this roller-coaster ride of a podcast with your guide through this maze, joined by two titans of the trade—Omar Arif of ClaimDOC & Scott Schnaidt of HST. They've both cracked the code, each in their unique ways, and the results? Nothing short of spellbinding.

🎯 What's on Tap:

The gears and levers behind RBP

Navigating the legal minefields

Secrets from Third-Party Administrators (TPAs)

RBP's performance across the geographical board

The art of handling balance bill claims

Litigation: When & How Often

Co-fiduciaries: The real deal or just smoke and mirrors?

Show Me the Money: Their pay structure dissected

Year-end Report Cards: The Good, the Bad, and the Profitable

And just when you think it couldn’t get any cooler—did one of these guys actually play pro baseball in a global tourney, while the other rocked the stage with NIRVANA? 🎸⚾

Lock in your earbuds. Prepare for a mind-bending journey. You’re entering "The Repricers"—Healthcare’s Final Frontier! 🌌🛸

I spent one morning this week chatting with Armstrong and Getty regarding the news that the federal government will finally begin negotiating the price of drugs. 10 of them. Two and a half years from now.

Your health insurance costs and premiums have skyrocketed compared to the rate of inflation since Obamacare passed. Meanwhile, insurance carrier stock prices have grown by 1900% in the same timeframe.

"They're making unimaginable amounts of money... off of you." -Joe Getty

Craig Gottwals, aka "Craig the Healthcare Guru,” talks about that and more in a new episode of A&G's Extra Large Podcast.

Listen to the Armstrong & Getty Extra Large Podcasts featuring Craig.

Turns out, insurers don’t have to decrease spending to make money. They just have to accurately predict how much the people they insure will cost. That way they can set premiums to cover those costs — adding about 20 percent for their administration and profit. If they’re right, they make money. If they’re wrong, they lose money. But, they aren’t too worried if they guess wrong. They can usually cover losses by raising rates the following year.

Frank suspects he got dinged for costing Aetna too much with his surgery. The company raised the rates on his small group policy — the plan just includes him and his partner — by 18.75 percent the following year.

The Affordable Care Act kept profit margins in check by requiring companies to use at least 80 percent of the premiums for medical care. That’s good in theory but it actually contributes to rising health care costs. If the insurance company has accurately built high costs into the premium, it can make more money. Here’s how: Let’s say administrative expenses eat up about 17 percent of each premium dollar and around 3 percent is profit. Making a 3 percent profit is better if the company spends more.

It’s like if a mom told her son he could have 3 percent of a bowl of ice cream. A clever child would say, “Make it a bigger bowl.”

Wonks call this a “perverse incentive.”

“These insurers and providers have a symbiotic relationship,” said Wendell Potter, who left a career as a public relations executive in the insurance industry to become an author and patient advocate. “There’s not a great deal of incentive on the part of any players to bring the costs down.”

Remember that “rule” in Obamacare that required all your preventive care and annual health exams be "free?" It was a blissful notion conjuring up unicorns flying across the sky, sprinkling fairy dust from their rainbow-colored stethoscopes.

We told employers and employees then - don’t count on it. First of all, nothing is ever free. The new law simply meant that all the preventive care you were supposed to get in a given year, would now be pre-paid with higher premiums. In other words, if you did not go to the doctor each year and maximize all of the preventive care that would be appropriate for someone of your health, age, and sex, you’d now be overpaying as all of our premiums increased by about 1 percent to cover the government mandated pre-payment racket.

So, how is this manifesting as double payment for many folks?

All our premiums went up 1% to prepay for it; and

If you aren't a hyper-diligent health-bill-nazi, you're likely being double-billed now when your doctor’s office keys in that you had a preventive exam as well as discussion, follow-up on, or evaluation of X. Where “X” can be any ailment, bump, sore, cut, tick, twitch, stressor, or annoyance in your life.

Our medical system even has a procedural code for “bitten by duck, initial encounter.” It is W61.61XAICD-10, in case you’d like your physician’s office to use it on your next visit. Please, if you do, don’t confuse that code with being “struck by a duck.” That is code W61.62. There are 155,000 codes in the ICD-10 system, in case you were wondering. And yes, because I know it is burning in the back of your mind as you read my scintillating post, there are codes for subsequent encounters with ducks as well; and for mere “contact” with a duck. U.S. Healthcare has ducks covered. But Cornish game hens? Not so much. In that case, you’d have to go with “pecked by chicken,” under ICD-10 code W61.33.

To say that our system has been bureaucratized beyond recognition into some sort of Frankenstein monster of public-private plunder is an understatement.

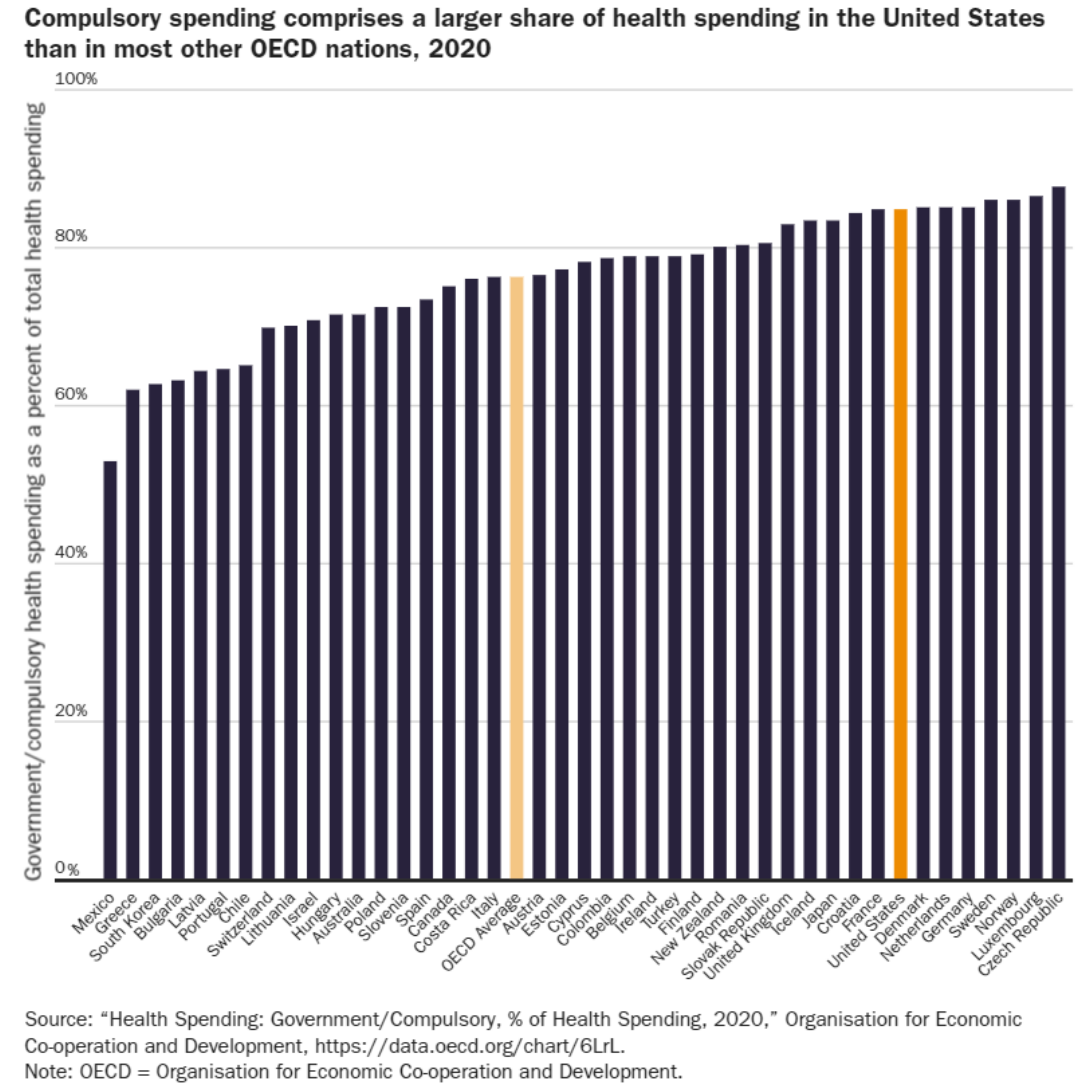

The government controls a larger share of health spending in the United States (85%) than in 30 other advanced nations, including Canada (75%) and the United Kingdom (83%), each of which has explicitly socialized health systems.Source.

So, are preventive visits pre-paid and copay-free under Obamacare? Only if you have impeccable health and you and your doctor do not discuss your blood pressure, blood glucose levels, sun exposure, moles, sniffles, or whether you’ve been pecked by a Cornish game hen. Of course, some doctors get it and are more forgiving than others. There are cases where you can get away with your depraved, thieving ways and attempt to get free healthcare advice during your purely preventive visit by asking about that odd little bump that’s appeared in your nether regions. Bandit!

Real-world advice: if your doctor asks you if there is anything else bothering you in your physical, and it is something minor about which you were mildly curious, say, “yes, I do have another question, but it is kind of a silly one and I don’t want to be billed for moving our visit beyond a purely preventive visit.”

A good doctor will gladly answer your question and not bill you. If your doctor doesn’t roll that way, it’s a decent sign that you may need a new doctor.

Now, if the issue is large enough that you want to discuss it and don’t care if it goes on for a few minutes, then by all means, ask. But know that your free exam just moved into an office visit for which you will pay a copay, co-insurance, or the visit cost if you are on a high-deductible health plan. But what would you rather do, finish this visit for free and then return in a few weeks to address the burning topic? If you do that, you’re doubling your time and will still pay for the visit.

Here is how Yahoo News covered this new phenomenon that’s been around for more than a decade (highlights are mine):

‘I got scammed’: Americans describe getting surprise medical bills via health care loopholes

Sometimes a simple coding mishap can result in a major headache for a patient, as was the case for Anthony, a 29-year-old based out of Norwalk, Conn.

When Anthony visited his doctor for a routine annual checkup — which his insurance plan through Cigna advertised as 100% covered without a copay — he ended up receiving a bill for $132.09.

This was because his doctor’s office coded the visit as an “office visit” instead of an “annual checkup or preventative care.” In an effort to clear up the confusion, Anthony called both Cigna and his doctor’s office, and Cigna assured him that it was simply listed under the wrong code and would be covered if the doctor’s billing department corrected it.

“I submitted a complaint to Westmed, and they forwarded it to the billing department,” Anthony told Yahoo Finance. “They rejected my request several times. According to them, the office staff had the final word on the billing code. I was able to talk to the office staff directly too, but I’m not sure who was responsible for selecting the billing code there.” …

“Wasted a bunch of time, and, frankly, I got scammed," Anthony said. "In the end, I got no explanation why they used the wrong code, and the bill was sent to collections. It’s going to hurt my credit score and in the U.S., that also means my ability to find a place to rent or even buy a house if I ever get the chance. It’s the kind of thing you lose sleep over.”

'They think short-term'

A loophole in the ACA — commonly known as Obamacare — is part of the reason why this issue persists in the U.S.

Under the ACA, insurers are required to cover preventive services such as cancer screenings, immunizations, and well-woman visits without cost-sharing, meaning that the individual receiving the services is not required to pay anything.

A study published in 2021 in the journal Preventive Medicine found that “in addition to premium costs meant to cover preventive care, Americans with employer-sponsored insurance were still charged between $75 million and $219 million in total for services that ought to be free to them.” …

Not-so-free procedures

Because of these loopholes, patients often find themselves billed for routine procedures that typically are fully covered by their health insurance.

Several individuals, who asked to remain unnamed due to privacy concerns, shared with Yahoo Finance the forms they were required to sign in order to be seen for routine physicals and other preventive exams.

In one of the forms, an individual was told that if they discussed any new or chronic medical issues with their doctor, their insurance would be billed for both an office visit and a preventive health exam.

For another individual, their form indicated that if they discussed new acute conditions or a worsening chronic condition, if a diagnostic test was ordered, or if a treatment changed, they would also be subject to two separate bills.

“There are a lot of gray areas but generally, those shouldn’t be billed,” Jenifer Bosco, a staff attorney at the National Consumer Law Center, told Yahoo Finance. “In the worst case, some providers do engage in what’s referred to as upcoding where they will try to bill for things or get reimbursed at a high rate for things that really should be either preventive or should be billed at a lower rate.”

For example, a preventive colonoscopy meant to screen for cancer is required to be covered at 100% by health insurance providers. However, if a polyp is discovered and removed from the patient during that screening, that procedure becomes a “surgery” rather than a screening and is billed as such.

“It makes zero sense charging the cost of something or the cost to the patient for something while they’re literally mid-procedure,” Bosco said. “You can essentially bill two visits for the same time, which I think intuitively just doesn’t make a lot of sense to most people. If you’re going in for one visit, how can you be charged for two and also be losing that free preventive visit at the same time?”

According to the Preventive Medicine study, patients were saddled with a total of $12.8 million for preventive colorectal screenings in 2018, while wellness visits incurred charges of up to $73.1 million.

“It feels a little bit like a bait and switch, and that’s not on the doctors,” Shafer said. “That’s just how we’ve set up the reimbursement guidelines and everything else. It’s frustrating.”

My first question was, who is calling for this?

Health insurers or property and casualty insurers, or both?

Turns out it is not the

traditional health insurance market, but accident insurers. I think of accident

insurers as more closely aligned with property and casualty since they pay you

for harm done after the fact instead of covering medical costs as you go. But it doesn’t matter for this analysis; I

just found that interesting.

With young people

spending an increasing amount of time in their own home, the umbrella

association of statutory accident insurers in Germany last year called

for more playgrounds that teach children to develop 'risk competence.’

Insurance lets you purchase a

piece of mind for risks that make you uncomfortable. Ideally, it is for risks you know you cannot cover

alone. Of course, it is also used for

risks that would be too painful to cover, such as if it required you to sell

your home or your fist born. I always start there. Most

white-collar folks who make more than $100K annually should buy the highest

deductible they can stomach for home and auto insurance.

Furthermore, unless an employer

pays for all or most of it, there is no need for dental or vision

insurance. Those are risks we can assess and should have enough savings

to cover. Paying an insurer to do so inserts a middleman, pays them

a profit and leaves you worse off.

What do we need? Medical and

disability insurance. We also may need life insurance if we have

dependents. Eventually, you should get to a point in life where you no

longer need it. I.e., kids out of college, home paid off, some savings in

the bank. At that point, your dependents will be fine with your

assets.

My second question was: why do German accident, property,

and casualty insurers want Germans to be better with risk? My initial

instinct tells me that this was against their interests. Snowflakes

who grow up cringe harder and fear more. Thus, they will buy more

insurance, even if it is irrational. And that generates larger profits

for insurers. But then I realized I was likely thinking too

long-term. Publicly traded corporations

may talk in terms of three to five-year plans, but in reality, they had better

show growth this quarter lest they want to get a public spanking.

The article does go on to state, "children

who had improved their motor skills in playgrounds at an early age were less

likely to suffer accidents as they got older." That does lead one to

believe that this is about profitability. But I still don't fully buy

it. Why? Because as soon as they begin to see more accidents due to

a wincing, flaccid populace, they can justify higher premiums and make more

profit.

Granted, property and casualty

insurers use different loss ratios than health insurers, but the following

analogy illuminates the point. In

America, it is widely accepted that insurers can make a modest and reasonable

profit at an 87% loss ratio. That means the insurer pays 87 cents in

claims for every dollar collected in premium, leaving 13 cents on the dollar to

pay salespeople, train staff, hire administrative folks, pay rent, and pay taxes.

Obamacare's Perverse Unintended

Consequence

In 2009 and 2010, legislators

decided it would be a good idea to regulate the profitability of health

insurers in America. To those ends, Obamacare mandates that large

insurers maintain loss ratios of 85% or more. If not, they must rebate a

portion of the premium to policyholders. The minutia of how those numbers

are calculated and disbursed is mind-numbing, so I'll spare you that here.

This effectively means insurers will

only retain 15 cents on the dollar. And

from that 15 percent, they must pay all business costs. If they miss and come in at an 82% loss ratio

in their state, they must rebate 3% to get to 85%. If they underwrite incredibly lean (and never

do) and hit an 88% loss ratio, they may not even make enough to cover

costs. To be sure, it’s a small eyelet

to thread.

So how does Purple Cross make more

money in this environment? With more

claims, of course! If I only get to keep

15% of a pie, I’d much prefer a billion-dollar pie to a million-dollar

one. So yeah, have at it employer and

employees. Run up as many claims as you

want. We’ll jack premiums and eat

more. Oh, and for good measure, Purple

Cross can also cut things like fraud detection and customer service

training. Those simply eat away at the

15%, and the U.S. market is already an oligopoly, so where will you run to, Mr.

Consumer? Purple Shield, Green Cross,

how about Emperor Wilhelm?

Back to Deutschland

What is really going on in

Germany? I’m not entirely sure. If I take my tinfoil hat off and make an

effort to be altruistic (just for a minute, Ayn. It’s just a thought

experiment!) I might conclude that the

German insurers are genuinely doing what they think is best for their

nation. I mean, it is still possible for

mega-corps to do the right thing for the right thing’s sake, isn’t it?

Just kidding. It is likely something a little deeper. Actuarial tables are complex sets of data

tasking actuaries and, eventually, underwriters with the “art” of assessing

risk. Yeah, it is more of an art than a

science, as much as they want you to believe it is perfectly cold and

calculated. Don’t get me wrong. Their job is, as my buddy Gary would say, “harder than a whore’s

heart.” But there is so much wiggle room

in there that if policyholders knew how the sausage was made, they’d likely go

vegan. And don’t think for a minute

government actuaries do any better. For

example, when Medicare and Medicaid first passed in 1965, government bean

counters told us it would cost $12 billion by 1990. In reality, it was $110 billion.

“Missed

it by that much.”

More recently, Obamacare

originally had long-term care insurance embedded within. But the reality on that line of coverage is

that folks are living so much longer now, in old folks’ homes and in need of

continual care, that the industry still has not come up with a reliable way to

assess this risk. Hence, congress repealed Obamacare’s LTC program before it ever got off

the ground. Californitopia also recently

eliminated its LTC coverage in CalPERS.

The point is, as much as I want to

believe insurers can simply raise premiums to cover increased risk, it’s not

something that easily happens overnight.

And the one thing that insurers hate more than anything is … the

unknown. If they can’t measure and

assess it, they pull the product or jack the rates so high that nobody wants to

buy. Obamacare cemented that trick for American

health insurers:

“If

You Like Your Plan, You Can Keep Your Plan

Sure, you can keep it so long as

you can afford the premium increases, your employer doesn’t change carriers,

and your carrier continues to offer the same obsolete plan even though they are

now required, in every state, to license a whole new litany of plans that comply

with Obamacare’s mandated bloat. Easy

peasy.

The Patient Disruption and

Unaffordable Care Act made a rule that mandated insurers always renew coverage

at year’s end. Pre-2010, your insurer

could cancel you if you had an epically bad year. Obamacare fixed that. Now, carriers issue 75% renewal increases to

accomplish the same thing. Problem

solved.

Conclusion(s)

I’m left with three possible conclusions as I

ponder this story:

1.(1) If German

accident insurers operated under the same warped, public-private partnership (i.e.,

fascistic)

rules as Obamacare, not only would those insurers display indifference toward greater

childhood risk-ignorance, they would foster it. That would lead to more claims and be the only

way German insurers could generate more revenue in the future. Again, 15% of a billion is much better than 15%

of a million. Aren’t price controls

neat?

2.(2) Enough

cynicism. Let me white pill this for a moment.

It is certainly possible that the insurers want what is best for Germany.

And, as they look across the pond to

their WWII liberators, they see what happens when you fastidiously bubble-wrap

your youth in endless layers of protection. It’s not good. Good times are definitely

creating weak men. So, at least on its

face, there is an argument that the Deutschlanders are solely doing what is

right for their youth.

3.(3) This

brings me to my third and most likely conclusion. Germany’s carriers are horrified at the speed

at which the namby-pamby are changing risk calculus. Hence, Germany’s plea to allow more risk and

play on more dangerous playgrounds is more likely tied to the bottom line. It is not our Obamacare analogy or altruism;

instead, it is most like our U.S. long-term care calculus. In their eyes, if people become more paranoid

and want to buy more coverage for perceived risks, great. But let’s not do this overnight because we still

must have some clue as to how to underwrite our precious little snowflakes in

the short term. For a carrier, claim

expansion is great for business over the long haul if it is predictable and can

be ushered in with higher premiums. But the

market will topple when the claims skyrocket in a short enough period (like 1

to 3 years).

Alas, this third conclusion is actually

the scariest. Accident insurers (at

least in Germany) are signaling that the wussification of our youth is

happening so fast, they are not confident in their ability to profit from

it. It’s bad enough that we

bubble-wrapped our snowflakes as we hover over them in helicopters to ensure

nothing bad ever happens. But we’re doing

it so fast that the oligarchs and the oligopoly are worried that our degradation

will infringe upon their ability to plunder from our demise.

California Expands Who an Employee Can Care for Under the CFRA and California Paid Sick Leave Law - "Beginning January 1, 2023, employees throughout California will be able to use sick leave or take leave under the California Family Rights Act (CFRA) to care for a 'designated person' ... defined as any individual related by blood or whose association with the employee is equivalent to a family relationship. An employee can designate this person at the time they request leave."

California Unleashes Last-Minute Onslaught of New Employment Legislation - California Governor Newsom recently signed several pieces of employment-related legislation into law including: Supplemental Paid Sick Leave Extension, an expansion of the California Family Rights Act and California Paid Sick Leave, Unpaid Bereavement Leave, Emergency Working Conditions, Reproductive Health Decisionmaking, and Cal/WARN Act Enforcement for Call Centers.

In 2021, the U.S. health care system spent $603 billion on prescription drugs, before accounting for rebates, of which $421 billion was on retail drugs.

Spending growth on drugs was largely due to growth in spending per prescription, and to a lesser extent by increased utilization (i.e., more prescriptions).

Expenditure growth was larger for non-retail drug expenditures (25%) than for retail expenditures (13%).

Between 2016 and 2021, the location where people received their drugs changed. Americans increasingly received their drugs from mail order pharmacies (35% increase), clinics (45% increase), and home health care (95% increase). During the same time period, there were decreases in drugs received through independent pharmacies (5% decrease), long term care facilities (17% decrease), and federal facilities (9% decrease).

Drug spending is heavily driven by a relatively small number of high-cost products. The cost of specialty drugs has continued to grow, totaling $301 billion in 2021, an increase of 43% since 2016. Specialty drugs represented 50% of total drug spending in 2021. While the majority (80%) of prescriptions that Americans fill are for generic drugs, brand name drugs accounted for 80% of prescription drug spending in both retail and non-retail settings, with little change over time. The top 10% of drugs by price make up fewer than 1% of all prescriptions but account for 15% of retail spending and 20%-25% of non-retail spending.

Prescription drug spending trends have been less affected by the COVID-19 pandemic than health care services.

Several provisions in the Inflation Reduction Act address drug pricing, including allowing the Secretary of HHS to negotiate prices in Medicare Parts B and D for selected medications and introducing Medicare rebates for drug prices that rise faster than inflation. These provisions may impact future drug spending trends.

Telemedicine was made easy during COVID-19. Not any more- "Over the past year, nearly 40 states and Washington, D.C., have ended emergency declarations that made it easier for doctors to use video visits to see patients in another state, according to the Alliance for Connected Care, which advocates for telemedicine use. Some, like Virginia, have created exceptions for people who have an existing relationship with a physician. A few, like Arizona and Florida, have made it easier for out-of-state doctors to practice telemedicine. Doctors say the resulting patchwork of regulations creates confusion and has led some practices to shut down out-of-state telemedicine entirely. That leaves follow-up visits, consultations or other care only to patients who have the means to travel for in-person meetings."

Health and Wellness

Sore Throat, Now the Most Common Sign of COVID - "where once a fever and loss of taste or smell were early warning signs of the bug, the symptom tracking app has revealed the most common symptoms have changed."

People who sleep 5 hours or less a night face a higher risk of multiple health problems as they age - "The study, published Tuesday in the journal PLOS Medicine, took a closer look at a group of nearly 8,000 civil servants in the United Kingdom who had no chronic disease at age 50. Scientists asked the participants to report on how much sleep they got during clinic examinations every four to five years for the next 25 years. For those whose sleep was tracked at age 50, people who slept five hours or less a night faced a 30% higher risk that they would develop multiple chronic diseases over time than those who slept at least seven hours a night. At 60, it was a 32% increased risk, and at 70, it was a 40% greater risk."

One thing employers need to keep in mind as they ponder the addition of a vaccine mandate on employees and the implementation surcharges/penalties against employees who refuse the jab is that additional penalties assessed against the employee could push the employer's plan over PPACA's affordability limits. This would trigger a $4,060 fine back against the employer for each impacted employee. Kyle Scott, writing over at Benefits Pro summarizes this nicely here:

The Affordable Care Act (ACA) requires Applicable Large Employers (ALEs) to offer affordable health care benefits to eligible employees or pay a penalty. Within the ACA law lie very specific rules governing the design of wellness programs, especially regarding incentives and penalties (premium surcharges). ...

In 2021, affordability is achieved when an employee’s cost for health insurance benefits is no more than 9.83% of that employee’s household income. This percent is adjusted each year and safe harbors apply. ...

If the cost including the surcharge renders the plan as unaffordable, and the employee goes to the exchange and receives a premium tax credit, the employer may be subject to Penalty B. The $4,060 penalty per year can be multiplied by the total number of full-time employees who did not have an offer of affordable coverage and who also receive a premium tax credit. ...

While there is an exception for tobacco, there’s nothing currently in the ACA rules that similarly applies to a surcharge or penalty for non-COVID-19 vaccinated employees. ...

I visited with Jack and Joe this morning to discuss the latest NYT article on how the Trump Administration's transparency regulations are starting to shed some light on the absolute absurdity of American healthcare pricing. We originally discussed these regulations in 2019 here and here. As the NYT notes, this is a very rare bipartisan effort for regulators and legislators - at least on the surface. But we have a long way to go to make these rules more effective.

Our discussion was cut off before I could answer that last question. The answer is yes. We are still on a path toward some sort of socialized medicine by the end of the 2020s. We cannot sustain this present system much longer.

Yet Medicare, the US’s largest single government-funded program only increases its payment by less than 1% per year.

This leaves large medical systems highly pressured to increase what they negotiate as reimbursement from BUCA (Blues, UHC, Cigna & Aetna – Big 4).

In 2010 Obamacare added a price control to healthcare mandating that insurers like the Big 4 may not keep more than 15% as profit and overhead. I.e., Insurers must prove that they are spending 85% of every dollar we give them on claims as opposed to overhead and profit.

This is called the “MLR” Mandate (Medical Loss Ratio).

The impact of this was to relax insurers’ incentive to keep claim costs down. Why? Because the only way for an insurer to increase revenue is to glow the claims pie. 15% of a $4,000 MRI pays better than 15% of a $1,000 MRI.

So now when giant hospital systems want to inflate prices for any given set of procedures, insurers have a reduced incentive to naturally fight against that inclination because of the bureaucracy.

"Since many of the administrative costs in health insurance are hard to cut out—costs like fraud prevention—insurers will be forced to resort to another option to meet Obamacare’s MLR mandates: premium hikes.

Think of it this way: let’s say you’re charging $10,000 for a health plan, and have $7,000 of health costs associated with that plan (and $3,000 of administrative costs), for an MLR of 70 percent. If you want to increase your MLR to 80%, there are two ways to do it. First, you can cut administrative costs and premiums (if administrative costs were $1,750, and premiums $8,750, $7,000 of health costs would equal an 80% MLR). Second, you can keep your administrative costs the same ($3,000 per person), and find ways to spend more money on health-care, passing on the costs in the form of premium hikes ($15,000 in premiums, and $12,000 in health expenses, would also yield an MLR of 80%).

To put this another way: if an insurer is forced to choose between cutting administrative costs by 42 percent, or not firing its employees and instead hiking premiums by 50 percent, which is it going to choose? After all the fat is trimmed, the insurer is going to choose to increase premiums, and increase them significantly. It will spend money on wasteful health expenditures, the kind that liberal health wonks are always complaining about, just to meet an arbitrary MLR target."

In addition to this, the excessive regulation and government involvement have made it increasingly difficult to have smaller, nimble, price-competitive medical systems and insurers.

And about 16 enormous hospital chains. We’ve moved from a “free market” to a highly bureaucratized oligopoly.

Doctors are not the problem. Individual practitioners are being overrun by this government-healthcare industrial complex nearly as quickly as patients are. Our largest challenges in this area are:

The government;

Insurers;

The pharmaceutical industry; and

Large hospital chains and medical groups

What can we do?

Encourage your congressman to:

support these transparency regulations and legislative efforts;

increase the penalties for hospital failures to disclose the pricing information; and

Employers must look to use smaller, local insurers. Employers with more than 300 to 500 employees should look to self-fund their health plans and remove insurers from the equation entirely. Reference base price your plan if you can.

If you think the federal budget situation in the United States is bad, and it is, you needn’t look any further than the remarkably inefficient and miserably managed systems of Medicare and Medicaid in order to get an idea of just how bad. As of today, our national debt is over $28 Trillion or $225,000 per taxpayer. But of course, that doesn’t take into account America’s unfunded liabilities. You know, how big that debt is when you factor in what we owe and have not set aside for Medicare, Medicaid and Social Security. After factoring that in, the real U.S. debt is $162 Trillion and each citizen owes $492,000.

This trick has actually been going on since the 1990s. Yup ... the 90s.

What is the problem? One-third of all government healthcare payments are wasted on fraud and abuse.

SeeCATO: In 2005, the New York Times reported that New York’s Medicaid program “has become so huge, so complex and so lightly policed that it is easily exploited,” and that “a chief state investigator of Medicaid fraud and abuse in New York City said he and his colleagues believed that at least 10 percent of state Medicaid dollars were spent on fraudulent claims, while 20 or 30 percent more were siphoned off by what they termed abuse, meaning unnecessary spending that might not be criminal.“

Medicare is now set to run out of money by 2023 or 2024.

SeeKaiser Health News: "The Committee for a Responsible Federal Budget, a nonpartisan group of budget experts focused on fiscal policy, estimates that the pandemic will cause the Part A Trust Fund to be unable to pay all of its bills starting in late 2023 or early 2024. “But we’re still very close,” said Marc Goldwein, the group’s senior vice president."

Even more problematic, healthcare expenditures continue to grow at 6% annually. Federal legislators look at this quandary and don't know what to do. Obviously the fraud can't be removed or it would have been over the last 30+ years. Yet, House and Senate members must still "bring home the bacon" to cement reelection. So how do they pass new legislation, particularly as it relates to healthcare, without totally blowing up the Congressional Budget Office's (CBO's) financial projections? Two tricks:

They write a provision into their favorite federal spending laws, like Obamacare, that provide that part of the way they will "fund" the new entitlements will be to cut the Medicare reimbursements to doctors by 2% per year. That way the "law" is in the books and the CBO must score the law assuming the cuts will happen.

Then, as those cuts come due, congress delays or suspends them. Every. Single. Time. Below is the latest story on this topic.

To reiterate the whole-scale financial negligence of the situation: one-third of U.S. government healthcare is waste, fraud and abuse. That same system compensates doctors less than half of what private plans do. But when congress is faced with how to make it more efficient or to save money, its answer is to bluntly cut the reimbursement to doctors even further because they know that the federal bureaucracies simply cannot get a handle on waste, fraud and abuse.

Of course when Medicare is paying less than half of what employer-based plans pay and Medicaid pays 28% less than Medicare, nobody who wants to be re-elected will actually further reduce those reimbursements. Doing so would be political suicide.

The House on Tuesday approved a bill that would put off automatic cuts to Medicare provider payments until the end of the year.

The bill passed with a strong bipartisan majority of 384-38.

Technically, the House vote comes nearly two weeks after the cuts were set to take effect, but the delay came with knowledge that action could be postponed until Congress returned from recess and passed the legislation.

The automatic cuts were originally put into place by the 2011 Budget Control Act, which set up an annual 2 percent reduction in Medicare payments as one of its mechanisms for reducing the debt. Congress has never allowed the cuts to take place, however, voting to overturn them regularly over the past decade.

When Congress passed the CARES Act, its $2.2 trillion emergency COVID-19 bill, last March, it pushed the cuts off until April 1 as a way of countering some of the bill's costs, at least on paper. ...