It is good to see the legacy media covering an issue we began warning clients about more than a decade ago. Better late than never, I suppose.

Remember that “rule” in Obamacare that required all your preventive care and annual health exams be "free?" It was a blissful notion conjuring up unicorns flying across the sky, sprinkling fairy dust from their rainbow-colored stethoscopes.

We told employers and employees then - don’t count on it. First of all, nothing is ever free. The new law simply meant that all the preventive care you were supposed to get in a given year, would now be pre-paid with higher premiums. In other words, if you did not go to the doctor each year and maximize all of the preventive care that would be appropriate for someone of your health, age, and sex, you’d now be overpaying as all of our premiums increased by about 1 percent to cover the government mandated pre-payment racket.

So, how is this manifesting as double payment for many folks?

- All our premiums went up 1% to prepay for it; and

- If you aren't a hyper-diligent health-bill-nazi, you're likely being double-billed now when your doctor’s office keys in that you had a preventive exam as well as discussion, follow-up on, or evaluation of X. Where “X” can be any ailment, bump, sore, cut, tick, twitch, stressor, or annoyance in your life.

Our medical system even has a procedural code for “bitten by duck, initial encounter.” It is W61.61XAICD-10, in case you’d like your physician’s office to use it on your next visit. Please, if you do, don’t confuse that code with being “struck by a duck.” That is code W61.62. There are 155,000 codes in the ICD-10 system, in case you were wondering. And yes, because I know it is burning in the back of your mind as you read my scintillating post, there are codes for subsequent encounters with ducks as well; and for mere “contact” with a duck. U.S. Healthcare has ducks covered. But Cornish game hens? Not so much. In that case, you’d have to go with “pecked by chicken,” under ICD-10 code W61.33.

To say that our system has been bureaucratized beyond recognition into some sort of Frankenstein monster of public-private plunder is an understatement.

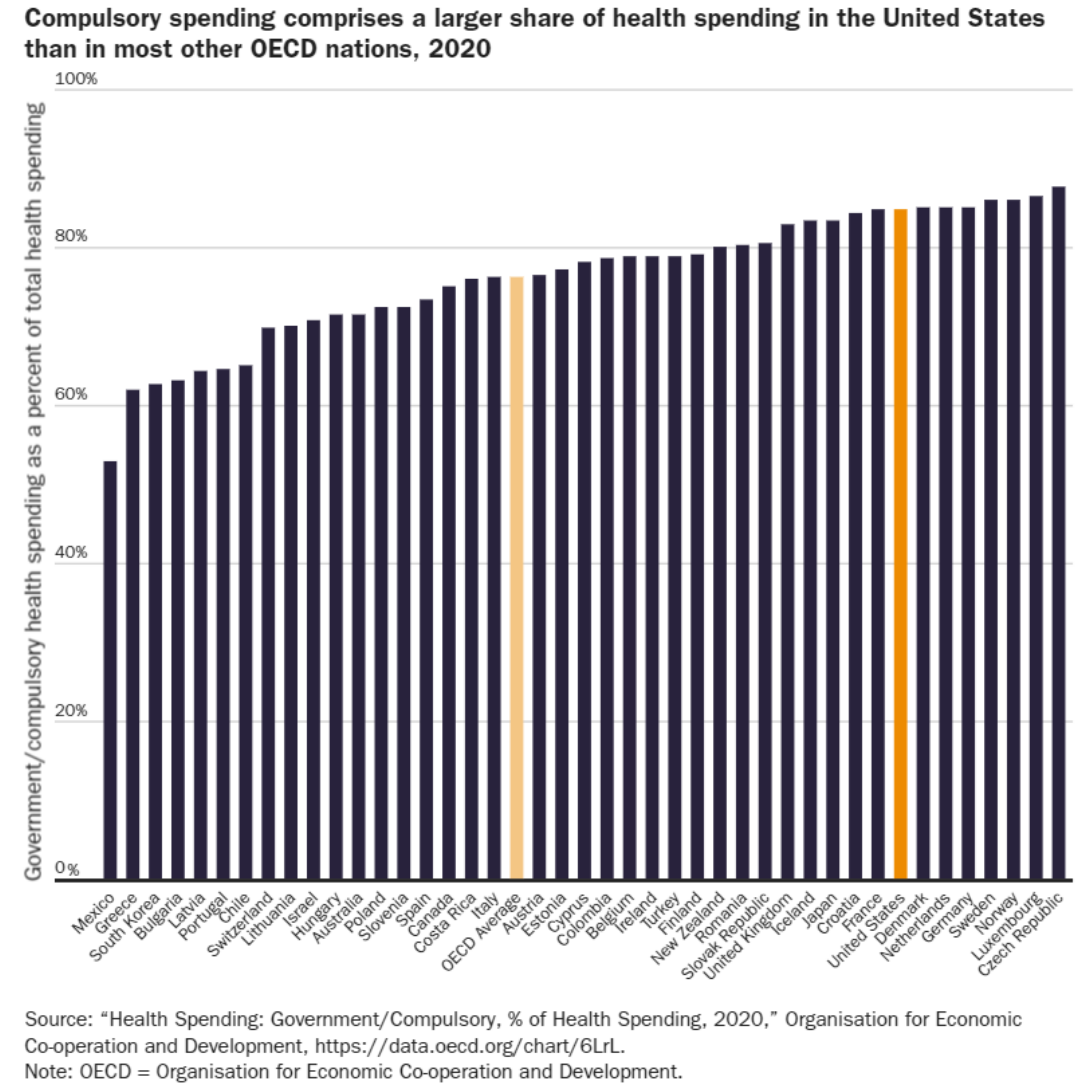

The government controls a larger share of health spending in the United States (85%) than in 30 other advanced nations, including Canada (75%) and the United Kingdom (83%), each of which has explicitly socialized health systems. Source.

So, are preventive visits pre-paid and copay-free under Obamacare? Only if you have impeccable health and you and your doctor do not discuss your blood pressure, blood glucose levels, sun exposure, moles, sniffles, or whether you’ve been pecked by a Cornish game hen. Of course, some doctors get it and are more forgiving than others. There are cases where you can get away with your depraved, thieving ways and attempt to get free healthcare advice during your purely preventive visit by asking about that odd little bump that’s appeared in your nether regions. Bandit!

Real-world advice: if your doctor asks you if there is anything else bothering you in your physical, and it is something minor about which you were mildly curious, say, “yes, I do have another question, but it is kind of a silly one and I don’t want to be billed for moving our visit beyond a purely preventive visit.”

A good doctor will gladly answer your question and not bill you. If your doctor doesn’t roll that way, it’s a decent sign that you may need a new doctor.

Now, if the issue is large enough that you want to discuss it and don’t care if it goes on for a few minutes, then by all means, ask. But know that your free exam just moved into an office visit for which you will pay a copay, co-insurance, or the visit cost if you are on a high-deductible health plan. But what would you rather do, finish this visit for free and then return in a few weeks to address the burning topic? If you do that, you’re doubling your time and will still pay for the visit.

Here is how Yahoo News covered this new phenomenon that’s been around for more than a decade (highlights are mine):

‘I got scammed’: Americans describe getting surprise medical bills via health care loopholes

Sometimes a simple coding mishap can result in a major headache for a patient, as was the case for Anthony, a 29-year-old based out of Norwalk, Conn.

When Anthony visited his doctor for a routine annual checkup — which his insurance plan through Cigna advertised as 100% covered without a copay — he ended up receiving a bill for $132.09.

This was because his doctor’s office coded the visit as an “office visit” instead of an “annual checkup or preventative care.” In an effort to clear up the confusion, Anthony called both Cigna and his doctor’s office, and Cigna assured him that it was simply listed under the wrong code and would be covered if the doctor’s billing department corrected it.

“I submitted a complaint to Westmed, and they forwarded it to the billing department,” Anthony told Yahoo Finance. “They rejected my request several times. According to them, the office staff had the final word on the billing code. I was able to talk to the office staff directly too, but I’m not sure who was responsible for selecting the billing code there.” …

“Wasted a bunch of time, and, frankly, I got scammed," Anthony said. "In the end, I got no explanation why they used the wrong code, and the bill was sent to collections. It’s going to hurt my credit score and in the U.S., that also means my ability to find a place to rent or even buy a house if I ever get the chance. It’s the kind of thing you lose sleep over.”

'They think short-term'

A loophole in the ACA — commonly known as Obamacare — is part of the reason why this issue persists in the U.S.

Under the ACA, insurers are required to cover preventive services such as cancer screenings, immunizations, and well-woman visits without cost-sharing, meaning that the individual receiving the services is not required to pay anything.

A study published in 2021 in the journal Preventive Medicine found that “in addition to premium costs meant to cover preventive care, Americans with employer-sponsored insurance were still charged between $75 million and $219 million in total for services that ought to be free to them.” …

Not-so-free procedures

Because of these loopholes, patients often find themselves billed for routine procedures that typically are fully covered by their health insurance.

Several individuals, who asked to remain unnamed due to privacy concerns, shared with Yahoo Finance the forms they were required to sign in order to be seen for routine physicals and other preventive exams.

In one of the forms, an individual was told that if they discussed any new or chronic medical issues with their doctor, their insurance would be billed for both an office visit and a preventive health exam.

For another individual, their form indicated that if they discussed new acute conditions or a worsening chronic condition, if a diagnostic test was ordered, or if a treatment changed, they would also be subject to two separate bills.

“There are a lot of gray areas but generally, those shouldn’t be billed,” Jenifer Bosco, a staff attorney at the National Consumer Law Center, told Yahoo Finance. “In the worst case, some providers do engage in what’s referred to as upcoding where they will try to bill for things or get reimbursed at a high rate for things that really should be either preventive or should be billed at a lower rate.”

For example, a preventive colonoscopy meant to screen for cancer is required to be covered at 100% by health insurance providers. However, if a polyp is discovered and removed from the patient during that screening, that procedure becomes a “surgery” rather than a screening and is billed as such.

“It makes zero sense charging the cost of something or the cost to the patient for something while they’re literally mid-procedure,” Bosco said. “You can essentially bill two visits for the same time, which I think intuitively just doesn’t make a lot of sense to most people. If you’re going in for one visit, how can you be charged for two and also be losing that free preventive visit at the same time?”

According to the Preventive Medicine study, patients were saddled with a total of $12.8 million for preventive colorectal screenings in 2018, while wellness visits incurred charges of up to $73.1 million.

“It feels a little bit like a bait and switch, and that’s not on the doctors,” Shafer said. “That’s just how we’ve set up the reimbursement guidelines and everything else. It’s frustrating.”