- Covered California anticipates an average increase of 4.2% on the exchange in 2015.

- Increases are artificially suppressed for three reasons:

- Three Rs taxpayer transfers to insurers;

- Last year's increases of up to 88%; and

- Insurer fear over California's proposed Proposition 45 which would empower state bureaucrats with premium oversight.

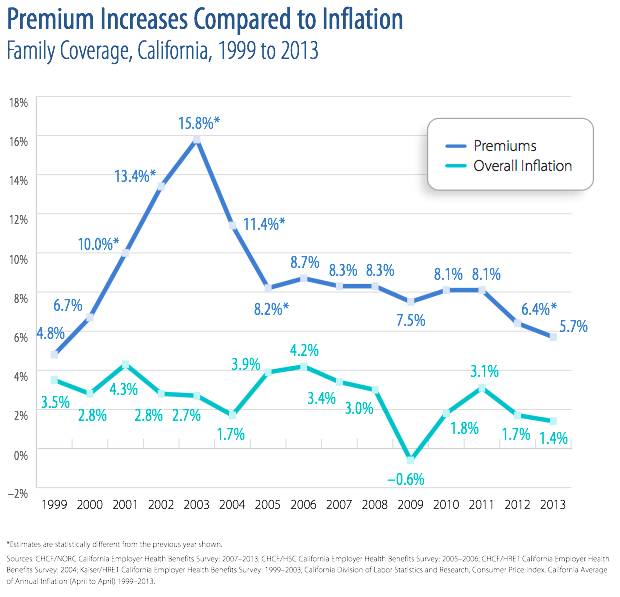

On Thursday, Covered California announced that the tentative, average renewal increase for plans sold on the state health insurance exchange will be 4.2% in 2015. This is great news for enrollees and employers. While the announced increase is not for employer-based plans, the early indicators are that we’ll also see lower than expected renewals in the employer insurance market. The below-discussed market forces will similarly impact group plans, albeit, not as directly as exchange plans. After about a decade and a half of renewals that doubled or tripled the consumer price index, this is a long awaited relief for the battered and weary.

Clearly, everybody wants to know if this is due to the Patient Protection and Affordable Care Act (PPACA or "Obamacare") and whether it will last. In short, yes, this is certainly at least partially a result of PPACA. And no, this will not be the new normal in health insurance renewals.

California Dreamin' - Milk, Honey and 4 Percent Renewals! Why?

California Dreamin' - Milk, Honey and 4 Percent Renewals! Why?

First and foremost we must not forget that PPACA exchange plans have a safety net mechanism built into them. The “Three R’s Program” (Risk adjustment, Reinsurance and Risk corridors, also referred to as the built in “bailouts”) is designed to channel taxpayer and profitable insurer money to insurers who lose money on exchange plans. Without getting too deep into the weeds, basically, an insurer will get back 50 percent to 80 percent of the dollars it loses on its exchange population during 2014, 2015 and 2016. The program terminates on its own after 2016.

This program is funded, in part, by a Transitional Reinsurance Tax we are all paying in our insurance plans. As news of the program finally made its way out into the mainstream in the late fall of 2013, political pressure mounted to revisit the propriety of such a program. On the heels of the bank bailouts and the mortgage crisis, the last thing a politician wants to do is defend taxpayer funds earmarked for insurers. That buzz startled insurers and the Administration. Neither of them can afford a repeal or congressional interference with the Three R’s Program. PPACA supporters downplayed the bailouts as a necessary, planned, and prudent way to smooth out what would be a possible rate shock when we add millions of uninsured and presumably less healthy to our risk pools. Insurers want to quietly receive these funds while calling as little attention to the topic as possible.

The first bailout statistics are in and as Investors Business Daily reports, "taxpayers [are] on the hook for as much as $1 billion in bailout money through the law's 'risk corridor' program, thanks largely to the administration's unilateral decision to expand it. Twelve out of the 15 insurance companies that provided information to [Congress] expect to get 'risk corridor' checks from the government to cover their losses this year. Just one expects to pay into the 'budget neutral' program."

Incidentally, premium subsidies transferred to individuals will amount to $12 billion this year, according to the Congressional Budget Office. Over the next decade, they'll add up to a staggering $855 billion. (Investors.com.)

Hence, we have insurers that are buoyed by taxpayer dollars for the next three years to offset all potential premium shortfalls. Simultaneously, insurers are highly motivated to keep their renewal numbers as low as possible in the first two-years of the Three R’s Program to minimize political pressure against the program. A repeal or block to Three R’s would cause significant trauma to ObamaCare, immediately.

2. Massive Increases in 2014

California’s increases in 2014 were between 22 percent and 88 percent for individuals according to the state’s Insurance Commissioner, Dave Jones. Not only were premiums increased dramatically, but doctor networks were cut equally sharply; approximately in half for most plans and carriers operating in the exchange. By extracting that much premium from policyholders last year and greatly restricting doctor choices this year, insurers do not need as much of an increase in 2015 to keep the program afloat.

In comparing the costs for 2013 to 2014 plans, Investors Business Daily noted that:

California voters will go to the polls in November and decide whether the state should have authority to approve and restrict carrier premium increases. The prospect of this horrofies carriers in the Golden State. Even in the absence of Obamacare, carriers would be willing to take losses in 2015 and keep premiums as low as they can stomach in order to avoid fanning the flames of premium regulation. In the face of a lower than expected 4.2 percent increase, the voters won’t be as motivated to pass Proposition 45.

Incidentally, premium subsidies transferred to individuals will amount to $12 billion this year, according to the Congressional Budget Office. Over the next decade, they'll add up to a staggering $855 billion. (Investors.com.)

2. Massive Increases in 2014

Even the cheap Bronze plans [in Covered California] were more expensive than what Californians could buy before ObamaCare. That wasn't just because rates for the young went up — a common defense used by ObamaCare fans. Rates for an ObamaCare Silver plan were 36% higher than last year for 55-year-olds in the Sacramento area, 75% higher in Fresno, and 38% in L.A., the commissioner's report shows.Finally, California's decision not to implement one of the President's proposed alterations to PPACA softened the blow this year. In December when the President was awarded PolitiFact's lie of the year for telling people they could keep their plan if they liked it, he attempted to change the law via press conference and permit people to keep non-compliant, less expensive insurance plans for one more year. California's declination of this offer to "de-un-grandfather" previously "un-grandfathered" plans helped to ensure that the initial rate-shock band-aid would be torn off all at once instead of over two years.

There is a highly contentious November ballot initiative facing the health plans they absolutely do not want to see passed, that would put the government in charge of their rate setting in future years, giving the carriers every incentive to low-ball the 2015 rates so voters don't have any more incentive to vote for it.

I don’t expect to see four percent renewals continue, but it looks like we are going to have at least a one-year reprieve from excessive premium escalation. Employers would be best served to take the savings this year and bank them while budgeting for 2016 and 2017's increases to be double or triple the amount we are likely to see in the employer market in 2015.

A version of this story was published at LifeHealthPro with permission.